Tapera's Big 2026 Play: How Indonesia's Housing Fund Is Betting on Longer Loans & Digital Speed

What

BP Tapera—Indonesia's housing finance body—is making moves. Over the past week, headlines show the organization pushing three main levers: extending FLPP (Fasilitas Likuiditas Pembiayaan Perumahan) loan terms up to 40 years, expanding into vertical housing, and migrating its SiKasep service onto a new mobile app. The occupancy rate for FLPP homes hit 94.02%, and the organization is coordinating with banks, ministries, and regional governments to hit 2026 targets.

Why it matters

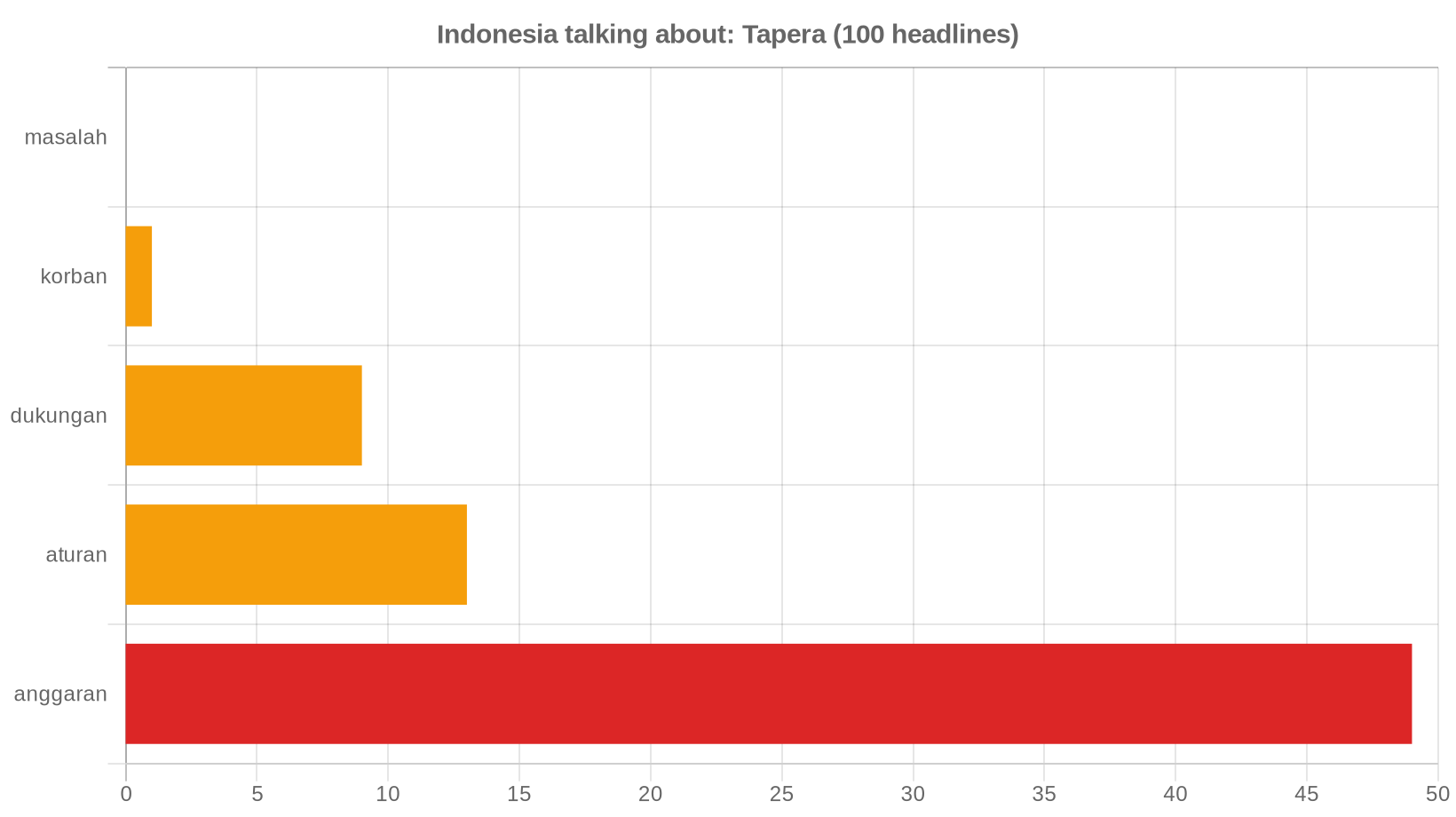

The budget/cost angle dominates the coverage (49 of 100 headlines analyzed). Longer loan terms mean lower monthly payments—a direct lever to make subsidized housing accessible to lower-income workers. The shift toward vertical housing and regional expansion (Nias, Kalbar, Surabaya) suggests Tapera is trying to solve the "last mile" problem: how to get subsidy programs into places and price points where they actually get used. The mobile app migration is less flashy but critical—it removes friction from the application process.

One wrinkle: the revised P2SK law will expand OJK oversight of Tapera and other housing funds, which adds a regulatory layer to watch.

Who it's for

First-time homebuyers in the lower-to-middle income bracket. FLPP subsidies are designed for workers earning up to a certain threshold; longer terms directly benefit them. Regional governments and property developers also matter here—they're co-signers on the coordination strategy.

When & where

This is now. Recent coverage (3 headlines in the past 7 days) shows active rollout. The SiKasep app migration is "resmi" (official). Regional pilots are live in Surabaya (KUR perumahan hit Rp305.26 billion), Palembang, Singkawang, and West Kalimantan. The 2026 targets are the deadline.

How

Tapera is using three tools:

- Loan term extension: Proposing 40-year FLPP terms for vertical housing—standard mortgages are typically 15–20 years.

- Digital acceleration: SiKasep (the old system) is now on Tapera Mobile, reducing paperwork friction.

- Stakeholder coordination: Tripartite agreements with banks, ministries, and regional partners to align incentives and reduce bottlenecks.

The "penghuni cadangan" (reserve occupant) strategy mentioned in one headline suggests Tapera is also thinking about demand-side nudges—pre-filling units to create social proof.

The takeaway

Tapera isn't waiting for 2026; it's building the infrastructure now. The focus on cost (longer terms), access (mobile app, regional expansion), and coordination (tripartite deals) suggests the organization has learned that subsidies alone don't move the needle—you need payment affordability, frictionless application, and trust-building. The 94% occupancy rate is a win, but the real test is whether the 40-year term and vertical-housing push can sustain that momentum in tighter markets. Watch the OJK oversight angle—it could tighten or loosen Tapera's operating room depending on how the revised P2SK law lands.

Note: This analysis is based on a read of recent news coverage (100 headlines analyzed, 3 in the past 7 days). It reflects what media outlets are reporting about Tapera's strategy and program metrics, not official government data.

Building an AI agent?

I'm packaging how I ship them into one kit. Early access:

AI Agent Starter Kit →