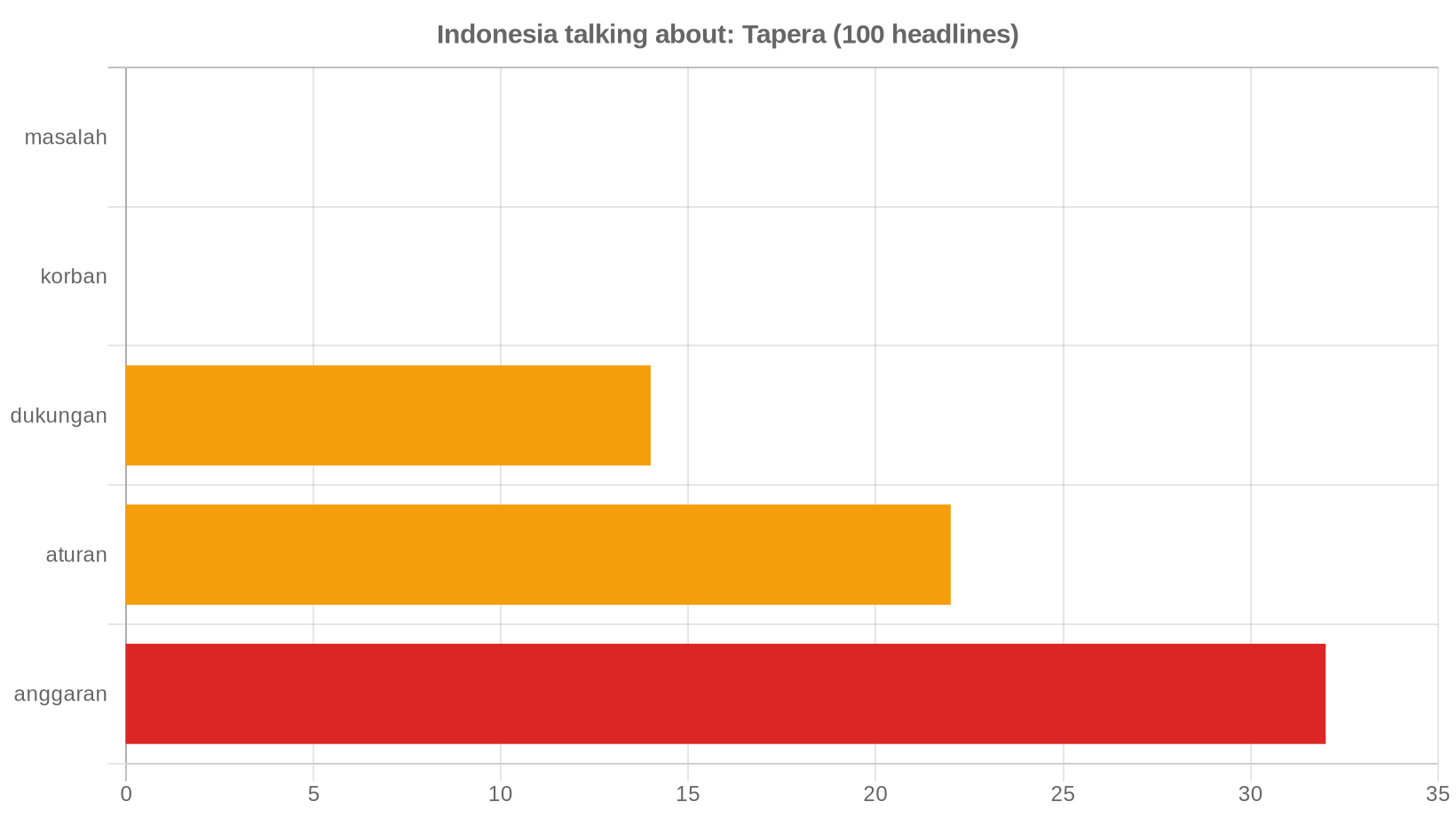

Tapera's 2026 Bet: 43 Banks & 259K+ Homes Already Delivered, Here's What's Actually Happening

What

BP Tapera just announced it's partnering with 43 banks to distribute FLPP (subsidy housing) loans in 2026. The program has already delivered 259,841 housing units, with occupancy hitting 94.02%. They're also migrating digital services (SiKasep) to a mobile app and strengthening ties with developers, ministries, and state enterprises.

Why it matters

Affordable housing is a chronic pain point in Indonesia. This isn't just bureaucratic shuffling, the coverage shows a deliberate scaling play. Tapera is betting on volume through partnerships rather than going it alone. The 43-bank network, digital migration, and cross-ministry coordination suggest they're trying to reduce friction in the loan approval and disbursement pipeline. Whether that actually speeds things up for borrowers is the real test.

Who it's for

ASN (civil servants), UMKM workers, and salaried employees in underserved regions like Nias, Kalbar, and Surabaya. The coverage emphasizes "subsidi" (subsidy) repeatedly, this is targeted at lower-income brackets, not the general market.

When & where

The 2026 push is live now, with recent announcements spanning late 2024 into early 2025. Geographic focus: Nias, West Kalimantan, Surabaya, Palembang, and other provincial areas. The BSPS (Bantuan Subsidi Perumahan Stabil) is slated to reach "all regions" by 2026.

How

Three-pronged approach:

- Bank partnerships: 43 lenders handling FLPP disbursement (up from prior years).

- Digital infrastructure: SiKasep app migration to Tapera Mobile; electronic certificates with BSSN for security.

- Stakeholder alignment: Tripartite agreements with ministries, developer associations, and state enterprises to vet quality and occupancy.

KUR Perumahan (housing credit) in Surabaya alone hit Rp305.26 billion, a concrete signal of capital flow.

The takeaway

Tapera is doing the unglamorous work: scaling distribution networks, digitizing paperwork, and locking in developer accountability. The 94% occupancy rate and 259K+ units suggest the machinery is moving. But recent headlines are all about policy coordination and bank expansion, not about borrower pain points or approval timelines. That gap matters. If you're waiting for a subsidy home, the infrastructure is being built; whether it actually reaches you faster remains an open question.

Building an AI agent?

I'm packaging how I ship them into one kit. Early access:

AI Agent Starter Kit →